Table of Contents

The Central Board of Secondary Education (CBSE) has published the Class 12 Accountancy sample paper 2024-25 on its official website. The CBSE Class 12 Accounts Sample Paper 2024-25 is precisely constructed to reflect the most recent CBSE exam pattern, ensuring that students are fully prepared for the real level exam. Students studying for forthcoming board exams can review the entire Class 12 Accountancy example paper 2024 25 with solutions provided on this page.

Class 12 Accountancy Sample Paper 2024-25

Accountancy is an important subject for students pursuing the Commerce stream in Class 12. Because the Accountancy course requires a lot of calculation, students must spend more on practicing. In this exercise, the recently released CBSE Class 12 Accountancy Sample Paper 2024-25 serves as an excellent practice resource. The Accounts sample paper Class 12 2024-25 will give CBSE Commerce stream students an idea of how to prepare based on the question paper pattern and the kind of questions asked in the sample paper. Thus, most of the students are advised to for through the official sample paper multiplier times to familiar with the real exam paper pattern.

CBSE Class 12 Accounts Sample Paper 2024-25 pattern

As earlier mentioned the Sample paper of the Class 12 Accountancy is completely based on the latest exam pattern and syllabus. Before moving to solve the paper, go through the pattern of the Class 12 Accountancy Sample Paper 2024-25 given below.

1. This question paper contains 34 questions. All questions are compulsory.

2. This question paper is divided into two parts, Part A and B.

3. Part – A is compulsory for all candidates.

4. Part – B has two options i.e. (i) Analysis of Financial Statements and (ii) Computerised Accounting.

Students must attempt only one of the given options.

5. Question 1 to 16 and 27 to 30 carries 1 mark each.

6. Questions 17 to 20, 31and 32 carries 3 marks each.

7. Questions from 21 ,22 and 33 carries 4 marks each

8. Questions from 23 to 26 and 34 carries 6 marks each

9. There is no overall choice. However, an internal choice has been provided in 7 questions of one mark, 2 questions of three marks, 1 question of four marks, and 2 questions of six marks.

Sample Paper of Accountancy Class 12 with Solution PDF 2024

CBSE Accountancy example question paper 2024 25 with solution in PDF format is available on CBSE Academic’s official website, cbseacademic.nic.in. To make things easier, we’ve provided a direct link to download the CBSE Accounts Sample Paper with Solutions PDf in the table below.

| Sample Paper of Accountancy Class 12 with Solution PDF 2024 Download Link | |

| Class 12 Accounts Sample Paper 2024-25 PDF | Click here |

| Marking Scheme and Solutions PDF | Click here |

Class 12 Accounts Sample Paper 2024-25 with Solutions

PART A

(Accounting for Partnership Firms and Companies)

1. Anthony a partner was being guaranteed that his share of profits will not be less than ₹ 60,000 p.a. Deficiency, if any was to be borne by other partners Amar and Akbar equally. For the year ended 31st March, 2024 the firm incurred loss of ₹ 1,80,000.

What amount will be debited to Amar’s Capital Account in total at the end of the year?

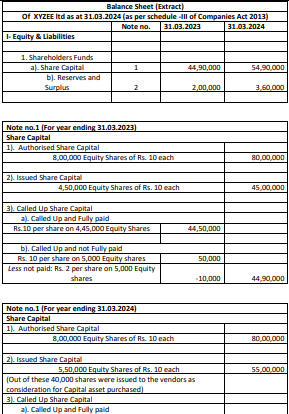

A. ₹ 60,000

B. ₹ 1,20,000

C. ₹ 90,000

D. ₹ 80,000

2. Assertion: Partner’s current accounts are opened when their capital are fluctuating.

Reasoning: In case of Fixed capitals all the transactions other than Capital are done through Current account of the partner.

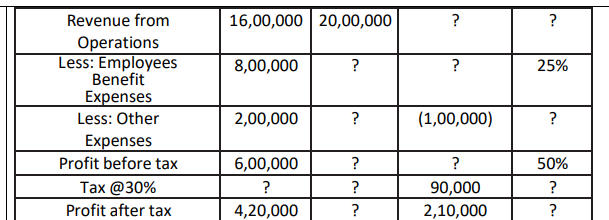

A. Both A and R are true and R is the correct explanation of A.

B. Both A and R are true but R is not the correct explanation of A.

C. A is true but R is false

D. A is false but R is true

3. Forfeiture of shares leads to reduction of _________________Capital.

A. Authorised

B. Issued

C. Subscribed

D. Called up

OR

Moon ltd. issued 40,000, 10% debentures of ₹100 each at certain rate of discount and were to be redeemed at20% premium. Exiting balance of Securities premium before issuing of these debentures was ₹12,00,000 and after writing off loss on issue of debentures , the balance in Securities Premium was ₹2,00,000. At what rate of discount these debentures were issued?

A. 10%

B. 5%

C. 25%

D. 15%

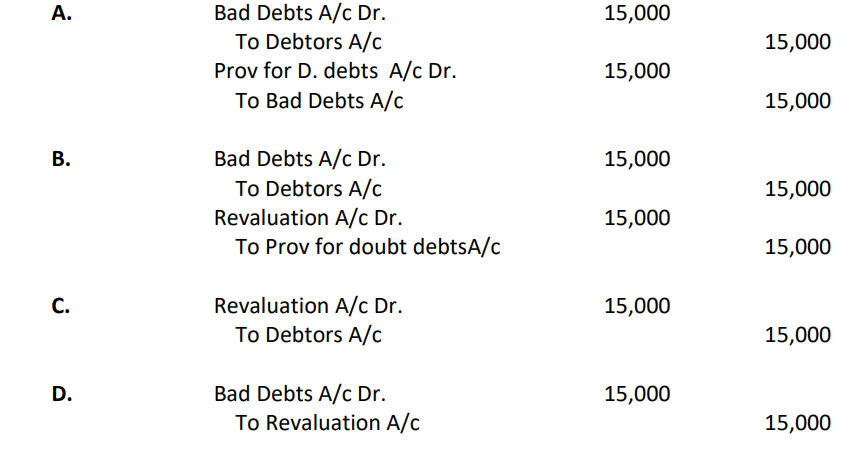

4. At the time of admission of new partner Vasu, Old partners Paresh and Prabhav had debtors of ₹ 6,20,000 and a provision for doubtful debts (PDD) of ₹ 20,000 in their books. As per terms of admission, assets were revalued, and it was found that debtors worth ₹ 15,000 had turned bad and hence should be written off. Which journal entry reflects the correct accounting treatment of the above situation?

OR

Ram and Shyam were partners sharing profits and losses in the ratio of 3:2. Their balance sheet shows the building at ₹ 1,60,000. They admitted Mohan as a new partner for 1/4th share. In additional information it is given that the building is undervalued by 20%.

The share of loss/gain of revaluation of Shyam is ____________ & current value of building shown in new balance sheet is _______.

A. Gain ₹ 12,800, Value₹ 1,92,000 B. Loss ₹ 12,800, Value₹ 1,28,000

C. Gain ₹ 16,000, Value₹ 2,00,000 D. Gain ₹ 40,000, Value₹ 2,00,000

5. The profit earned by a firm after retaining ₹ 15,000 to its reserve was ₹ 75,000. The firm had total tangible assets worth ₹ 10,00,000 and outside liabilities ₹ 3,00,000. The value of the goodwill as per capitalization of average profit method was valued as ₹ 50,000. Determine the rate of Normal Rate of Return.

A. 10 %

B. 5 %

C. 12 %

D. 8 %

6. Mohit had applied for 900 shares, and was allotted in the ratio 3 : 2. He had paid application money of ₹ 3 per share and couldn’t pay allotment money of ₹ 5 per share. First and Final call of ₹ 2 per share was not yet made by the company. His shares were forfeited. The following entry will be passed

Share Capital A/c Dr. X

To Share Forfeited A/c Y

To Share Allotment A/c Z

Here X, Y and Z are:

A. ₹ 6,000; ₹ 2,700; ₹ 3,300 B. ₹ 4,800; ₹ 2,700; ₹ 2,100

C. ₹ 4,800; ₹ 1,800; ₹ 3,000 D. ₹ 6,000; ₹ 1,800; ₹ 4,200

Or

A company forfeited 6,000 shares of ₹ 10 each, on which only application money of ₹ 3 has been paid. 4,000 of these shares were re-issued at ₹ 12 per share as fully paid up. Amount of Capital Reserve will be _______.

A. ₹ 18,000 B. ₹ 12,000

C. ₹ 30,000 D. ₹ 24,000

7. On 1st April 2019 a company took a loan of ₹80,00,000 on security of land and building. This loan was further secured by issue of 40,000, 12% Debentures of ₹100 each as collateral security. On 31st March 2024 the company defaulted on repayment of the principal amount of this loan consequently on 1st April 2024 the land and building were taken over and sold by the bank for ₹70,00,000. For the balance amount debentures were sold in the market on 1st May 2024. From which date would the interest on debentures become payable by the company?

A. 1st April 2019.

B. 31st March 2024.

C. 1st April 2024.

D. 1st May 2024.

8. Rama, a partner took over Machinery of ₹ 50,000 in full settlement of her Loan of ₹ 60,000. Machinery was already transferred to Realisation Account. How it will effect the Realisation Account?

| A. Realisation Account will be credited by | B. Realisation Account will be credited by |

| C. Realisation Account will be credited by | D. No effect on Realisation Account |

OR

Dada, Yuvi and Viru were partners sharing profits and losses in the ratio 3:2:1. Their books showed Workmen Compensation Reserve of ₹ 1,00,000. Workmen Claim amounted to ₹ 60,000. How it will affect the books of Accounts at the time of dissolution of firm?

A. Only ₹ 40,000 will be distributed amongst partner’s capital account

B. ₹ 1,00,000 will be credited to Realisation Account and ₹ 60,000 will be paid off.

C. ₹ 60,000 will be credited to Realisation Account and will be even paid off. Balance ₹ 40,000 will be distributed amongst partners.

D. Only ₹ 60,000 will be credited to Realisation Account and will be even paid off

9. Ikka, Dukka and Teeka were partners sharing profits and losses in the ratio of 2:2:1. Their fixed Capital balances were ₹ 5,00,000; ₹ 4,00,000 and ₹ 3,00,000 respectively. For the year ended March 31, 2024 profits of ₹ 84,000 were distributed without providing for Interest on Capital @ 10% p.a as per the partnership deed. While passing an adjustment entry, which of the following is correct?

A. Teeka will be debited by ₹ 4,200

B. Teeka will be credited by ₹ 4,200

C. Teeka will be credited by ₹ 6,000

D. Teeka will be debited by ₹ 6,000

10. At the time of dissolution Machinery appears at ₹ 10,00,000 and accumulated depreciation for the machinery appears at ₹ 6,00,000 in the balance sheet of a firm. This machine is taken over by a creditor of ₹ 5,40,000 at 5% below the net value. The balance amount of the creditor was paid through bank. By what amount should the bank account be credited for this transaction?

A. ₹ 60,000.

B. ₹ 1,60,000.

C. ₹ 5,40,000.

D. ₹ 4,00,000.

11. Rahul, Samarth and Ayaan were partners sharing profits and losses in the ratio of 5:4:3. Ayaan’s fixed Capital balance as on March 31, 2024 was ₹ 2,70,000. Which of the following items would have affected this Capital balance?

A. Profit/Loss for the year B. Additional Capital introduced

C. Reduction in Capital due to

Capital Adjustment

D. Both B and C

12. Shares issued as sweat equity can be

(I) Issued at par.

(ii) Issued at discount.

(iii) Issued at a premium.

Which of the following is correct?

A. Only (i) is correct.

B. Both (i) and (iii) are correct.

C. All are correct.

D. Only (ii) is correct.

13. 2,000 shares allotted to Ms. Regal, on which ₹ 80 each called up and ₹ 50 paid were forfeited and reissued for ₹ 70 each as ₹ 90 paid up. Amount transferred to capital reserve A/c is

A. ₹ 1,00,000 B. ₹ 60,000

C. ₹ 40,000 D. ₹ 20,000

14. Joey, Sam and Tex were partners sharing profits and losses in the ratio 5:3:2. W.e.f 01 April, 2024 they decided to share future profits and losses in the ratio 2:1:1. For which of the following balances Tex will be credited at the time of reconstitution of firm, if the firm decided to continue with available accumulated profits and losses balances.

A. General Reserve ₹ 2,00,000 and Profit and Loss (Dr.) ₹ 1,20,000

B. General Reserve ₹ 2,00,000 and Profit and Loss (Cr.) ₹2,50,000

C. Deferred Revenue Expenditure ₹ 50,000 and Profit and Loss (Cr.) ₹ 80,000

D. Deferred Revenue Expenditure ₹ 50,000 and Profit and Loss (Dr.) ₹ 80,000

15. Rohit, Virat, and Shikhar were partners sharing profits and losses in the ratio of 3:1:1. Their Capital balance as on March 31, 2024 was ₹ 3,00,000; ₹ 2,70,000 and ₹ 2,50,000 respectively. On the same date, they admitted Hardik as a new partner for 20% share. Hardik was to bring ₹ 80,000 for his share of goodwill and 1/5 of the combined capital of all the partners of new firm. What will be the total amount brought in by Hardik on his admission as a new partner?

A. ₹ 2,25,000 B. ₹ 1,80,000

C. ₹ 2,60,000 D. ₹ 3,05,000

OR

A, B and C were partners sharing profits and losses equally. B died on 31 August, 2023 and total amount transferred to B’s executors was ₹ 13,20,000. B’s executors were being paid ₹ 1,20,000 immediately and balance was to be paid in four equal semiannual instalments together with interest @ 10% p.a. Total amount of interest to be credited to B’s executors Account for the year ended March 31, 2024 will be?

A. ₹ 70,000 B. ₹ 67,500

C. ₹ 60,000 D. ₹ 77,000

16. String and Kite were partners sharing profits and losses in the ratio 5:3. They admitted spinner as a new partner. String sacrificed ¼ from his share and Kite sacrificed 1/6 of his share. What will be the new ratio?

A. 6:5:5 B. 9:5:10

C. 15:10:7 D. 35:21:40

17. Rusting, a partner of a firm under dissolution was to get a remuneration 2% of the total assets realized other than cash and 10% of the amount distributed to the partners. Sundry assets (including Cash ₹ 8,000) realized at ₹ 1,16,000 and sundry liabilities to be paid ₹ 31,340. Calculate Rustings’s remuneration and Show your workings clearly. Also, pass the necessary journal entry for remuneration.

18. A, B and C were partners sharing profits, and losses in the ratio of 2:2:1. C died on 1st July, 2023 on which date the capitals of A, B and C after all necessary adjustments stood at ₹74,000, ₹ 6,750 and 42,250 respectively. A and B continued to carry on the business for six months without settling the accounts of C. During the period of six months from 1 -7-2023, a profit of ₹ 20,500 is earned using the firm’s property. State

which of the two options available u/s 37 of the Indian Partnership Act, 1932 should be

exercised by executors of C and why?.

Or

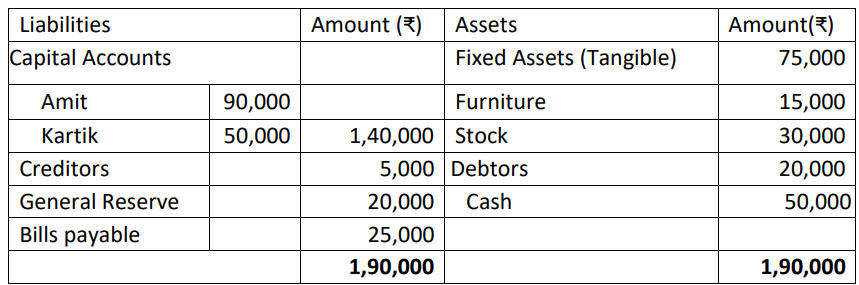

Amit and Kartik are partners sharing profits and losses equally. They decided to admit Saurabh for an equal share in the profits. For this purpose, the goodwill of the firm was to be valued at four years’ purchase of super profits. The Balance Sheet of the firm on Saurabh’s admission was as follows:

The normal rate of return is 12% p.a. Average profit of the firm for the last four years was ₹30,000. Calculate Saurabh’s share of goodwill.

19. Buddha Limited took over assets of ₹ 40,00,000 and liabilities of ₹ 6,50,000 of Ginny Limited. Buddha Limited issued 30,000, 8% Debentures of ₹ 100 each at 10% discount, to be redeemed at 5% premium along with a cheque of ₹ 5,00,000. Pass necessary journal entries in the books of Buddha Ltd.

Or

A company forfeited 8,000 shares of ₹ 10 each on which ₹ 8 were called (including ₹ 1 premium) and ₹ 6 was paid (including ₹ 1 premium). Out of these 5,000 shares were reissued at maximum possible discount. Pass necessary journal entries.

20. Bat, Cat, and Rat were partners sharing profits and losses in the ratio 5:3:2. Cat retired and on that date, there was a balance of Investment of ₹ 4,00,000 and Investment Fluctuation Reserve of ₹ 1,00,000 appearing in the balance sheet. Pass necessary journal entries for Investment Fluctuation reserve in the following cases.

(i) Market Value of Investments was ₹ 4,80,000.

(ii) Market Value of Investments was ₹ 3,80,000.

(iii)Market Value of Investments was ₹ 2,90,000

21. A company forfeited a certain number of shares of Face Value ₹ 10 each, for nonpayment of final call money of ₹ 4. These shares were reissued at a discount of ₹ 5 and the amount of ₹ 4500 was transferred to the capital Reserve account. Pass the necessary journal entries to show the above transactions and prepare a Share forfeited account.

22. X, Y, and Z were partners sharing profits and losses equally. Y died on 1st October, 2023 and the total amount transferred to Y’s executors was ₹ 15,60,000. Y’s executors were being paid ₹ 3,60,000 immediately and the balance was to be paid in four equal quarterly installments, together with Interest @ 6% p.a. Pass entries till payment of the first two installments.

23. K.N. Ltd. invited applications for issuing 6,00,000 equity shares of ₹10 each at a premium of ₹3 per share. The amount was payable as follows: On Application and Allotment – ₹3 per share; On First Call -₹4 per share; On Second and Final Call — Balance (including premium). The issue was oversubscribed by 1,50,000 shares. Applications for 50,000 shares were rejected and the application money was refunded. Shares were allotted to the remaining applicants as follows:

- Category I: Those who had applied for 4,00,000 shares were allotted 3,00,000 shares on pro- rata basis.

- Category II: The remaining applicants were allotted the remaining shares.

Excess application money received with applications was adjusted towards sums due on first call. Rakesh to whom 6,000 shares were allotted (out of Category I) failed to pay the first call money. His shares were forfeited. The forfeited shares were re-issued at ₹13 per share fully paid up after the second call. Pass necessary journal entries for the above transactions in the books of K.N. Ltd.

OR

a) Pass the necessary journal entries for ‘Issue of Debenture’ for the following:

- Arman Ltd. issued 750, 12% Debentures of ₹100 each at a discount of 10% redeemable at a premium of 5%.

- Sohan Ltd. issued 800, 9% Debentures of ₹100 each at a premium of 20 per debenture redeemable at a premium of ₹10 per Debenture.

b) X Ltd. obtained a loan of ₹4,00,000 from IDBI Bank. The company issued 5,000 9%. Debentures of ₹100 each as a collateral security for the same. Show how these items will be presented in the Balance Sheet of the company.

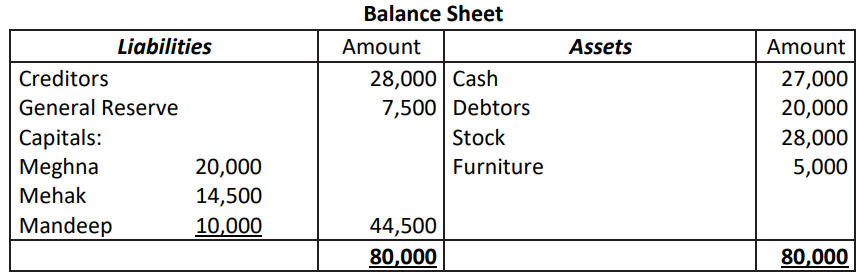

24. Meghna, Mehak and Mandeep were partnersin a firmwhose Balance Sheet as on 31st March, 2023 was as under:

Mehak retired on this date under following terms:

(i) To reduce stock and furniture by 5% and 10% respectively.

(ii) To provide for doubtful debts at 10% on debtors.

(iii) Goodwill was valued at `12,000.

(iv) Creditors of Rs.8,000 were settled at Rs.7,100.

(v) Mehak should be paid off and the entire sum payable to Mehak shall be brought in by Meghna and Mandeep in such a way thattheir capitalsshould be in their new profit-sharing ratio and a balance of Rs.25,000 is maintained in the cash account. Prepare Revaluation Account and partners’ capital accounts of the new firm.

Or

Varun and Vivek were partners in a firm sharing profits in the ratio of 3:2. The balance in their capital and current accounts as on 1st April, 2022 were as under:

| Particulars | Varun(₹) | Vivek(₹) |

| Capital accounts | 3,00,000 (Cr.) | 2,00,000 (Cr.) |

| Current accounts | 1,00,000 (Cr.) | 28,000 (Dr) |

The partnership deed provided that Varun was to be paid a salary of ₹ 5,000 p.m. whereas Vivek was to get a commission of ₹ 30,000 for the year. Interest on capital was to be allowed @ 8% p.a. whereas interest on drawings was to be charged @ 6% p.a.

The drawings of Varun were ₹ 3,000 at the beginning of each quarter while Vivek withdrew ₹ 30,000 on 1st September 2022. The net profit of the firm for the year, 2022-23, before making the above adjustments was ₹ 1,20,000. Prepare Profit and Loss Appropriation Account and Partners’ Capital and Current Accounts.

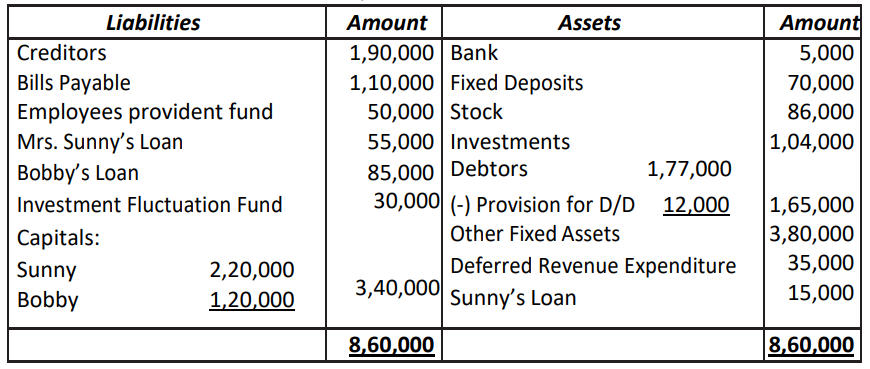

25. Sunny and Bobby were partners in a firm sharing profits and losses in the ratio of 3:2,

their balance sheet as of 31st March 2012:

The firm was dissolved on 31st March, 2012. The assets were realized and the liabilities were paid as under:

- Sunny promised to pay off Mrs. Sunny’s Loan

- Bobby took away stock at 20% discount and 80% of the investments at 10% discount.

- Dharam, a debtor of Rs. 60,000 had to pay the amount due 2 months after the date of dissolution. He was allowed a discount of 9% p.a. for making immediate payment.

- Creditors were paid Rs.1,75,000 in full settlement of their claim.

- 90% of Other fixed assets realized Rs. 1,98,000 and the remaining were realized at a discount of 15%.

- Balance of investments were sold at 75% value and Fixed Deposits were realised at 110%.

- There was an old piece of furniture which had been written off completely from the books, Bobby took away the same for Rs. 41,000 against his loan and the balance to him was given in cash.

- Realisation expenses of Rs. 20,000 were paid by Sunny and Bobby equally on behalf of the firm.

You are required to prepare Realisation A/c

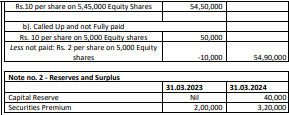

26.

During the year the company took over the business of Quipa Ltd. with Assets of Rs. 12,00,000/- and Liabilities of Rs.7,30,000. Purchase consideration was paid in cash and by issue of equity shares at par. The entire transaction resulted in Capital reserve of Rs.40,000.

Q1. What is the total face value of Shares issued for Cash by the Company during the year 2023-24.

A). Rs.10,00,000

B). Rs. 6,00,000

C). Rs. 9,50,000

D). Rs. 11,20,000

Q2. Shares issued for cash during the year were issued at _______. (assuming they were issued together)?

A). Rs.10

B). Rs.8

C). Rs.12

D). Rs.11.20

Q3. On April 1, 2024, the company forfeited all the defaulting shares. What amount will appear in the Share Forfeiture account at the time of forfeiture?

A). Rs.40,000

B). Rs. 50,000

C). Rs.10,000

D). Rs. 60,000

Q4. What will be the number of Issued shares, as on April 1,2024, after the forfeiture of these shares?

A). 5,45,000 shares

B). 5,50,000 shares.

C). 4,45,000 shares.

D). 5,05,000 shares.

Q5. If 2,000 of the forfeited shares were issued at Rs. 14 per share, what will be the amount of securities premium and Capital reserve respectively as on April 1, 2024?

A). Rs, 3,20,000, Rs.40,000

B). Rs.3,28,000, Rs.56,000

C). Rs.3,28,000, Rs.80,000

D). Rs.3,20,000, Rs.80,000

Q6. What will be the amount in the “Called up and Fully paid” subhead after the reissue of these 2000 shares?

A). Rs.54,50,000

B). Rs.55,00,000

C). Rs.54,70,000

D). Rs.54,80,000

Accounts Sample Paper Class 12 2024-25

Part B :- Analysis of Financial Statements

(Option – I)

27. When an analyst analysis the financial statements of an enterprise over a number of years, the analysis is called ______________analysis.

A. Static

B. External

C. Horizontal

D. Vertical

OR

————will result in an increase in Liquid Ratio without affecting the Current Ratio.

A. Sale of Stock at cost price

B. Sale of stock at loss

C. Sale of stock at profit

D. Sale of investments at cost

28. As on 31.02.2024 the following information of Bartan Manufacturing ltd. is available .

Net profit ratio 40%

Operating profit ratio 50%

On 1st April 2024 it came to notice that the accountant had omitted to record the interest received on an investment of Rs. 2,00,000 for the financial year 2023-24. The required rectification was done. What will be the effect of the same on Net Profit and operating profit ratio?

A. Net Profit ratio will increase and Operating Profit ratio will decrease

B. Both Net Profit ratio and Operating Profit ratio will increase

C. Net Profit ratio will increase and Operating Profit ratio will have no change

D. Net Profit ratio will remain same and Operating Profit ratio will increase

29. While computing cash from operating activities, which of the following item(s) will beadded to the net profit?

(i) Decrease in value of inventory

(j) Increase in share capital

(k) Increase in the value of trade receivables

(l) Increase in the amount of outstanding expenses

A. Only (i)

B. Only (i) and (ii)

C. Only (i) and (iii)

D. Only (i) and (iv)

OR

Which of the following statements is incorrect?

A. Investments in shares are excluded from cash equivalents unless they are in substantial cash equivalents.

B. Short-term marketable securities which can be readily converted into cash are treated as cash equivalents

C. In case of a financial enterprise, interest received and dividend received are classified as operating activities while dividend paid and interest paid are financing activities.

D. Dividend tax, i.e., tax paid on dividend should be classified as financing activity along with dividend paid.

30. Statement-I: ‘Shree Ltd.’ was carrying on a business of packaging in Delhi and earned good profits in the past years. The company wanted to expand its business and required additional funds. To meet its requirements the company issued equity shares of ₹30,00,000. It purchased a computerized machine of ₹20,00,000. During the current year the Net Profit of the company was ₹15,00,000. Cash flows from operating, investing and financing activities from the above transactions will be ₹15,00,000:

(₹20,00,000); ₹30,00,000 respectively.

Statement-II: The patents of X Ltd. increased from ₹3,00,000 in 2021-22 to ₹3,50,000 in 2022-23. It will be taken as purchase of Patents of 50,000 and will be shown under Cash outflow from Investing Activities.

A. Both the statements are true.

B. Both the statements are false.

C. Only Statement-I is true.

D. Only Statement-II is true.

31. Find the heads and sub-heads under which the following items will appear in the balance sheet of a company as per Schedule III, Part I of Companies Act, 2013?

a) Furniture and Fixture

b) Advance paid to contractor for building under construction

c) Accrued Income

d) Loans repayable on demand to Bank

e) Employees earned leaves payable on retirement

f) Employees earned leaves encash able

32. Complete the Comparative Statement of Profit and Loss:

| Particulars | 2022-23 | 2023-24 | Absolute change | % change |

|

||||

33. Calculate Gross Profit Ratio from the following information

Revenue from Operations ₹ 10,00,000; Purchases ₹ 3,60,000; Carriage Inwards ₹ 50,000; Employee benefit Expenses ₹ 1,00,000 (including Wages of ₹ 60,000); Opening Inventory ₹ 60,000 and Average Inventory ₹ 80,000.

OR

Profit after tax amounted to ₹ 6,00,000, and tax rate was 20%. If earnings before interest and tax was ₹ 10,00,000 and Nominal Value of Debentures amounted to ₹ 25,00,000 (assuming the only debt of the company), determine the rate of interest on debentures

34. (a) From the following information, calculate Cash flow from Operating Activities

Additional Information:-

Proposed Dividend for the year ended March 31, 2023 and March 31, 2024 was ₹ 1,50,000 and ₹ 1,80,000 respectively.

(b) From the following information calculate the Cash from Investing Activities

| Particulars | 31 March 2023 | 31 March 2024 |

| Machinery (Cost) | 20,00,000 | 28,00,000 |

| Accumulated Depreciation | 4,00,000 | 6,50,000 |

Additional Information:-

(i) Machinery costing ₹ 50,000 (Book Value ₹ 40,000) was lost by fire and insurance claim of ₹ 32,000 was received.

(ii) Depreciation charged during the year was ₹ 3,50,000.

(iii)A part of Machinery costing ₹ 2,50,000 was sold at a loss of ₹ 20,000.

Part B :- Analysis of Financial Statements

(Option – II)

27. The syntax of PMT Function is ___________

A. PMT (rate, pv, nper, [fv], [type])

B. PMT (rate, nper, pv, [fv], [type])

C. PMT (rate, pv, nper, [type], [fv])

D. PMT (rate, nper, pv, [type], [fv])

Or

In Excel, the chart tools provide three different options _________, _________ and __________ for formatting.

A. Layout, Format, DataMaker

B. Design, Layout, Format

C. Format, Layout, Label

D. Design, DataMaker, Layout

28. Which formulae would result in TRUE if C4 is less than 10 and D4 is less than 100?

A. =AND(C4>10, D4>10)

B. =AND(C4>10, C4<100).

C. =AND(C4>10, D4<10).

D. =AND (C4<10, D4,100)

29. Which function results can be displayed in Auto Calculate?

A. SUM and AVERAGE

B. MAX and LOOK

C. LABEL and AVERAGE

D. MIN and BLANK

Or

When navigating in a workbook, which command is used to move to the beginning of the current row?

A. [Ctrl]+[Home]

B. [Page Up]

C. [Home]

D. [Ctrl]+[Backspace]

30. What category of functions is used in this formula: =PMT (C10/12, C8, C9,1)

A. Logical

B. Financial

C. Payment

D. Statistical

31. State any three types of Accounting Vouchers used for entry. 3

32. State any three requirements which should be considered before making an investing decision to choose between ‘Desktop database’ or ‘Server database’.

33. State the features of Computerized Accounting system.

Or

Explain the use of ‘Conditional Formatting’.

34. Describe two basic methods of charging depreciation. Differentiate between both of them.

Computer Sample Paper Class 10 2025 with...

Computer Sample Paper Class 10 2025 with...

TN Inter Model Question Papers 2024-25, ...

TN Inter Model Question Papers 2024-25, ...

AP Inter Model Papers 2024-25, Download ...

AP Inter Model Papers 2024-25, Download ...